Tuesday, 15 July 2025

Written by MYTHEO

Key Takeaways

- Trump’s Megabill, signed July 4, 2025, marks a strategic policy pivot. It prioritizes capital and cuts welfare, a focused approach over broad economic expansion.

- Tax relief is selective: strong for businesses and high earners, but modest for most. Spending shifts to defense, bypassing infrastructure, and slashing key social programs.

- For investors: corporate tax breaks could fuel equities. Yet, rising debt pressures bonds with higher yields. Energy markets are split: negative for fossil fuels due to oversupply, but even more negative for renewables with direct incentive cuts.

While global tariffs continue to dominate headlines, President Trump's second term has introduced another sweeping policy move: the One Big Beautiful Bill Act, widely referred to as the "Trump Megabill." Signed into law on July 4, 2025, this expansive legislation brings significant changes across tax policy, federal spending, energy priorities, and social welfare programs.

A Look Back: The TCJA of 2017

During his first term, Trump’s signature legislative win was the Tax Cuts and Jobs Act of 2017 (TCJA). The law permanently lowered the corporate income tax rate from 35% to 21%, while allowing full expensing of business equipment purchases through 2022 to encourage capital investment.

On the individual side, the TCJA reduced tax rates across all income brackets, including a cut in the top marginal rate from 39.6% to 37%. However, these personal tax cuts were scheduled to expire after 2025.

Starting in 2022, the TCJA also changed how companies deduct research and development (R&D) costs, requiring amortization over five years instead of allowing immediate deductions. This shift has been especially unpopular among businesses focused on innovation and growth

Key Highlights of the Trump Megabill

Rather than introducing new taxes, the Trump Megabill offers a series of targeted incentives aimed at stimulating business investment and strengthening US competitiveness.

Key provisions include:

- Reinstatement of 100% bonus depreciation for equipment purchases

- Reversal of the TCJA’s R&D amortization requirement, allowing immediate deductions

- Expanded deductions for capital expenditures related to the construction of manufacturing facilities

These incentives apply retroactively to projects that began after January 19, 2025, and remain available for investments launched before January 1, 2029.

Impacts on Individual Taxpayers

On the personal tax front, the Megabill focuses on extending existing relief rather than introducing new cuts. The most notable change is the permanent extension of the 2017 tax rates. Without this measure, the top marginal rate would have reverted to 39.6% in 2026. Under the new law, it remains at 37%, preserving one of the most significant features of the original TCJA for high earners.

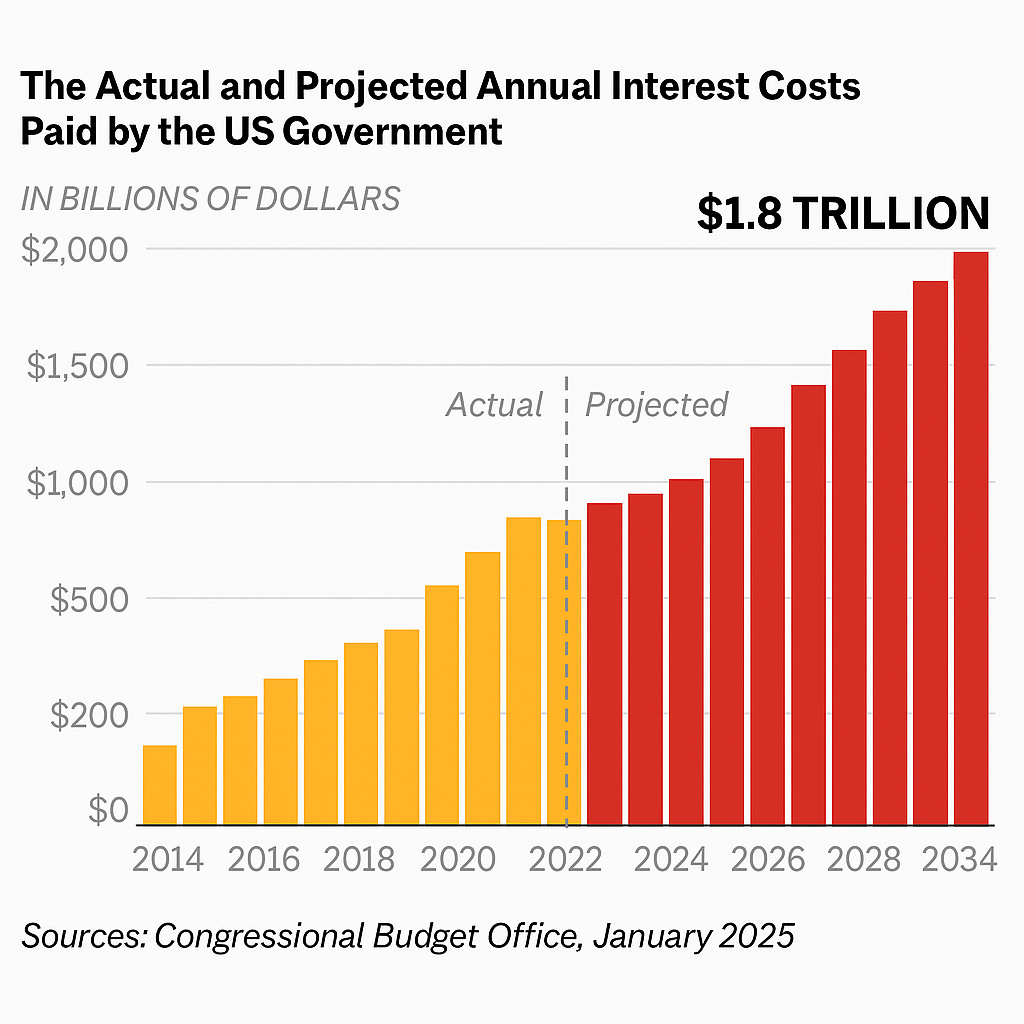

The Actual and Projected Annual Interest Costs Paid by the US Government

Sources: Congressional Budget Office (CBO), January 2025

Our Assessment: The Trump Megabill's Impact

Despite being billed as one big, beautiful piece of legislation, President Trump’s new “Megabill” lacks the economic punch of the 2017 tax cuts he championed during his first term. Back then, corporate taxes were slashed, and individuals across income levels saw meaningful reductions in their tax bills. That package had sweeping effects on both business investment and consumer confidence.

In contrast, the current bill offers more limited incentives. For businesses, it provides tax savings through deductions on equipment purchases, research and development, and factory construction. These targeted measures may help select industries, but they fall short of the broader stimulus seen in 2017.

On the personal tax front, there are no new reductions. Instead, the bill simply prevents the 2017 tax cuts from expiring and reverting to higher rates. Aside from a modest benefit for specific groups like tipped workers, most individuals will see little to no change in their tax burden.

What’s more concerning is the bill’s approach to spending. Rather than investing in infrastructure or broad-based economic initiatives, the focus is heavily skewed toward defense and border security. At the same time, the bill cuts billions from social safety net programs like Medicaid and SNAP. These moves reflect the administration’s political agenda but offer little to support overall economic growth or long-term productivity.

And while the bill adds to the spending ledger, it does nothing to address the most persistent threat to the US fiscal outlook: the growing budget deficit and rising national debt. For a bill that aspires to be monumental, in our point of view it misses the mark on solving the country real problem.